Making Your Pension and ISA Allowances Work for You

With tax thresholds frozen and inflation still higher than many households would like, more people are finding themselves paying more tax - sometimes without realising why.

The good news is that your pension and ISA allowances remain two of the most effective ways to improve tax efficiency and protect your savings.

Here’s a simple, practical breakdown of how they work and how to make the most of them.

Why Are More People Paying Higher Tax?

Several factors are combining to increase tax bills:

Frozen income tax thresholds (extended until 2031)

Wage growth pushing incomes higher

Inflation remaining above target

Changes announced in the Autumn Budget 2025

When tax bands stay the same but salaries rise, more income is pulled into higher tax brackets. This effect is often called “fiscal drag.”

It doesn’t just affect income tax. It can also reduce:

Your Personal Savings Allowance

Access to certain benefits

Your personal allowance if income exceeds certain limits

For example:

Basic rate taxpayers can earn £1,000 in savings interest tax-free.

Higher rate taxpayers see that fall to £500.

Additional rate taxpayers lose it entirely.

From April 2027, savings tax rates are also set to increase slightly, making tax-efficient wrappers even more valuable.

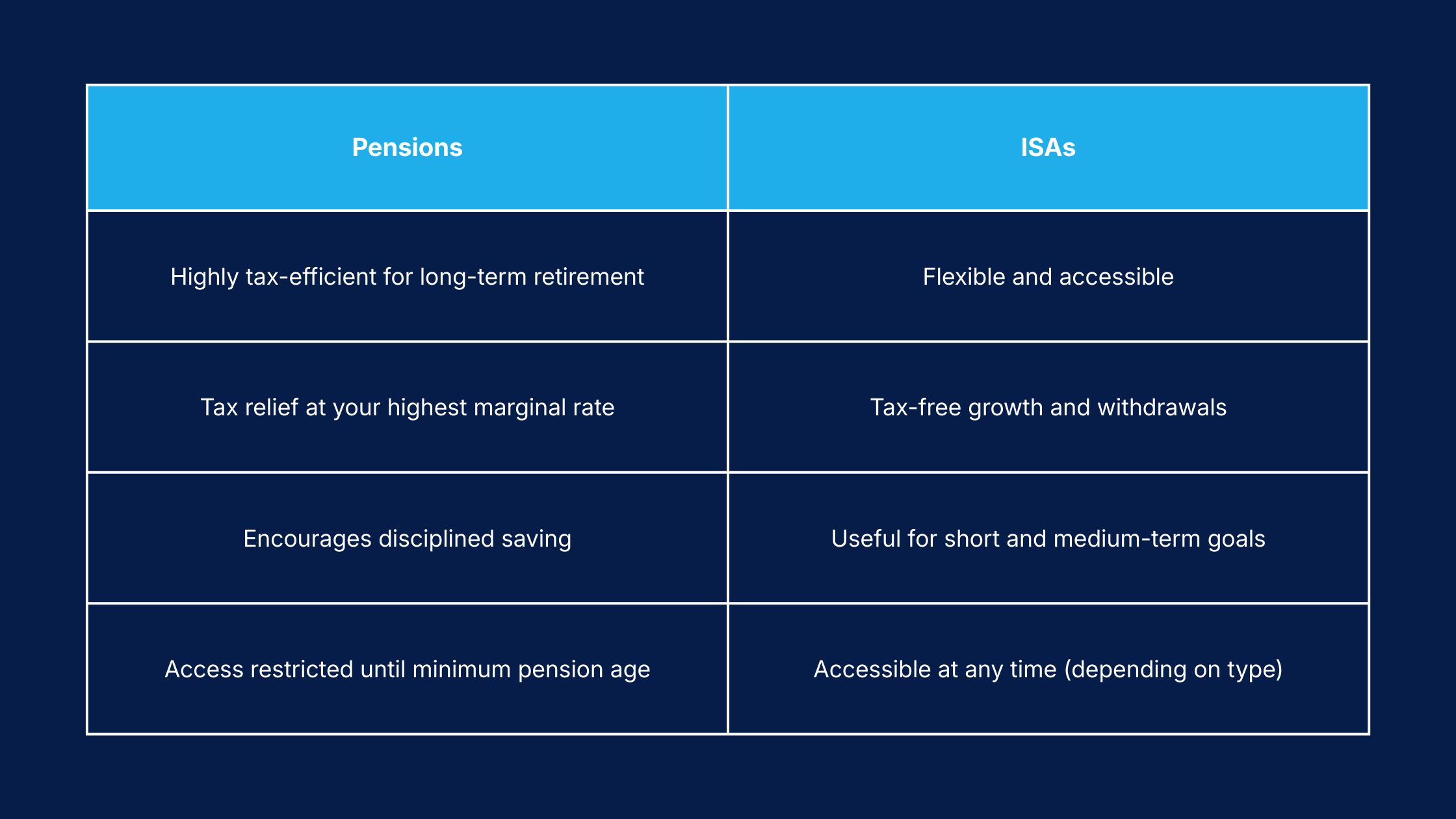

Pension Contributions - A Powerful Tax Tool

Pensions remain one of the most tax-efficient ways to save for the long term.

How Pension Tax Relief Works

When you contribute to a personal pension:

The pension provider automatically adds 20% basic rate tax relief

Higher or additional rate taxpayers can claim extra relief via HMRC

Contributions reduce your adjusted net income

Reducing adjusted net income can:

Help you stay within a lower tax band

Protect your personal allowance

Maintain eligibility for certain benefits

In many cases, a well-timed contribution before the tax year ends can make a noticeable difference.

Pension Contribution Limits

Annual allowance: £60,000 (for most people)

Tapered for incomes above £200,000 (down to £10,000 minimum)

Unused allowance can usually be carried forward for up to three tax years

Personal contributions are limited to 100% of earnings (or £3,600 if higher)

If you’ve started drawing certain types of pension income, lower limits may apply.

Long-Term Advantages of Pensions

Investments grow free from UK income tax and capital gains tax

Normally 25% of the fund can be withdrawn tax-free (subject to limits)

Designed for long-term saving

Accessible from age 55 (rising to 57 from April 2028)

Because funds are not easily accessed, pensions can help encourage disciplined long-term investing.

ISAs - Flexible, Tax-Efficient Saving

If pensions are powerful for retirement, ISAs are the flexible partner.

ISA Allowances

£20,000 annual allowance (use it or lose it)

Can be split across:

Cash ISAs

Stocks & Shares ISAs

Lifetime ISAs (if eligible)

Unlike pensions, unused ISA allowances cannot be carried forward.

Why ISAs Are So Popular

Money inside an ISA:

Grows free from income tax

Is free from capital gains tax

Can be withdrawn at any time (depending on ISA type)

Has no tax to pay on withdrawal

That flexibility makes ISAs useful for:

Medium-term goals

Emergency funds

Bridging income before retirement

Supplementing pension income later

Don’t Forget Junior ISAs

Junior ISA allowance: £9,000 per child

Funds grow tax-free

Accessible by the child at age 18

For couples maximising their own ISAs and a Junior ISA, that can mean a substantial amount sheltered from tax each year.

Budget 2025: Changes to Be Aware Of

The Autumn Budget 2025 announced future changes that may affect planning.

From April 2027:

Under-65s will be limited to £12,000 per year in a Cash ISA

Remaining ISA allowance must go into Stocks & Shares

Over-65s can still use the full £20,000 in cash if they wish

From April 2029:

National Insurance savings on salary sacrifice pension contributions will be capped at £2,000 per year

Income tax relief on pension contributions remains unchanged

While adjustments are coming, pensions and ISAs remain central to tax-efficient planning.

Pension or ISA - Which Should You Choose?

In many cases, the answer is both:

Holding a combination provides:

Flexibility over when and how you draw income

Control over tax in retirement

Greater resilience against future tax changes

Why Planning Matters

Spreading savings across pensions and ISAs can:

Improve overall tax efficiency

Reduce reliance on one income source

Provide more options later in life

Help manage risk across different investment types

Every individual’s situation is different. The right balance depends on income, goals, time horizon and attitude to risk.

Important Considerations

The value of investments can fall as well as rise. You may get back less than you invest.

A Stocks & Shares ISA does not provide the same capital security as a Cash ISA.

Inflation reduces the purchasing power of cash over time.

Tax rules and allowances can change and depend on individual circumstances.

Bringing It All Together

With frozen tax thresholds and evolving tax rules, making full use of your annual pension and ISA allowances has never been more important.

Used wisely, they can:

Reduce your tax bill today

Protect your savings from ongoing tax

Provide flexibility for the future

Support long-term financial security

If you’d like to review how your allowances are being used, speaking to a financial adviser can help ensure your strategy remains aligned with your goals.

Because good financial planning should allow you to save tax, and make your money work harder for you and your family.